India joins the worldwide search for a digital alternative to cryptocurrency

FROM BEING WARY OF BLOCKCHAIN AND cryptocurrencies until a few years ago, central banks across the world seem to have had a leap of faith: they are now zealously embracing the technology behind digital ledgers and programmable money. According to thinktank Atlantic Council’s programme titled “GeoEconomics Center”, 105 countries, representing over 95 per cent of the world’s GDP, are exploring the creation of Central Bank Digital Currencies (CBDCs), or digital currencies backed by each country, in order to provide an alternative amidst the growing popularity of cryptocurrencies worldwide.

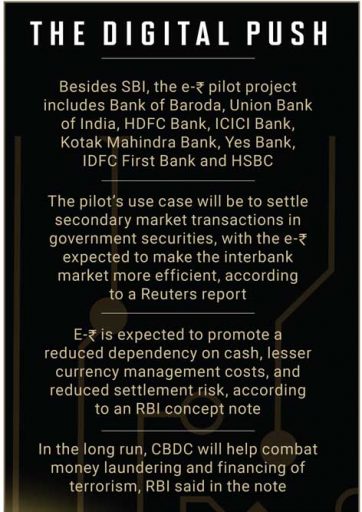

The Reserve Bank of India (RBI), which had brought out a concept note on October 7 over its plan to launch a digital currency using blockchain technology, also referred to as e-Rupee, inaugurated a pilot in the wholesale segment (e₹-W) on November 1. The RBI communiqué said that the use case for this pilot is the settlement of secondary market transactions in government securities, meaning it enables select business-to-business transactions. It added, “Use of e₹-W is expected to make the inter-bank market more efficient. Settlement in central bank money would reduce transaction costs by pre-empting the need for settlement guarantee infrastructure or for collateral to mitigate settlement risk. Going forward, other wholesale (business-to-business) transactions, and cross-border payments will be the focus of future pilots, based on the learnings from this pilot.”

As of now, nine banks—State Bank of India, Bank of Baroda, Union Bank of India, HDFC Bank, ICICI Bank, Kotak Mahindra Bank, Yes Bank, IDFC First Bank, and HSBC—have been identified for participation in this exercise. RBI said its pilot in the retail segment (e₹-R) will be launched in a month in select locations in closed user groups, comprising customers and merchants. According to RBI, on the first day of the pilot project, “the total number of trades settled in the government securities secondary market by using e₹-W was 48, amounting to ₹275 crore.” The central bank, meanwhile, did not respond to email queries from Open seeking details about their technology collaborations for the ongoing pilot project and whether it has enlisted support from crypto players.

So far, 11 countries have launched CBDCs, including eight countries in the eastern Caribbean region, the Bahamas, Nigeria, and Jamaica. The likes of China, Russia, South Africa, Singapore, Malaysia, and others have already kicked off their pilot schemes ahead of proposed launches. India, which had set up an internal working group under RBI in 2020, is also moving in that direction. Others, such as the US, economies in Europe and Australia, besides others, are either in development or research phases of developing central bank-backed digital money. Some central banks have tied up with crypto companies. For instance, the National Bank of Kazakhstan plans to integrate its digital currency into cryptocurrency exchange Binance’s BNB blockchain.

In its concept note, RBI said that like other central banks, it has also been exploring the pros and cons of the introduction of CBDCs. “The introduction of CBDC in India is expected to offer a range of benefits, such as reduced dependency on cash, lesser overall currency management cost, and reduced settlement risk. It could provide the general public and businesses with a convenient, electronic form of central bank money with safety and liquidity and provide entrepreneurs with a platform to create new products and services. The introduction of CBDC would possibly lead to a more robust, efficient, trusted, regulated and legal tender-based payments option (including cross-border payments),” the note said, emphasising that CBDC could also pose certain risks that may have a bearing on important public policy issues, such as risk to financial stability, monetary policy, financial market structure and the cost and availability of credit. “They need to be carefully evaluated against the potential benefits,” the note maintained. This report also said that the design of e₹ may be decided depending on the circumstances and the needs of the country. The internal high-level committee on CBDC was formed under the chairmanship of Ajay Kumar Choudhary, executive director, RBI, in February 2022 in order to “brainstorm and undertake an extensive study on various aspects of CBDC and explore the motivation for the introduction of CBDC, its design features and its implications on policy issues, choice of technology platforms, and accordingly suggest measures for its successful introduction.”

Prior to that, the Union Budget placed in Parliament on February 1 this year announced the creation of a digital rupee and stated that the introduction of CBDC will give a big boost to the digital economy.

THE RESPONSES TO CBDCs are mixed. A government official is optimistic about the pilot project that he says will “transform” towards a CBDC project that involves multiple countries. Atlantic Council highlights various such cross-border projects in the offing on its website. They include Multiple CBDC Bridge (mBridge), Project Dunbar, Project Helvetica, Project Jasper, Project Aber, Project Jura, and so on. Each of these involves multiple countries and banks. “I am sure central banks won’t lose out in the race for the future of money because of such initiatives,” the official avers.

Some others are opting to watch the scene cautiously.

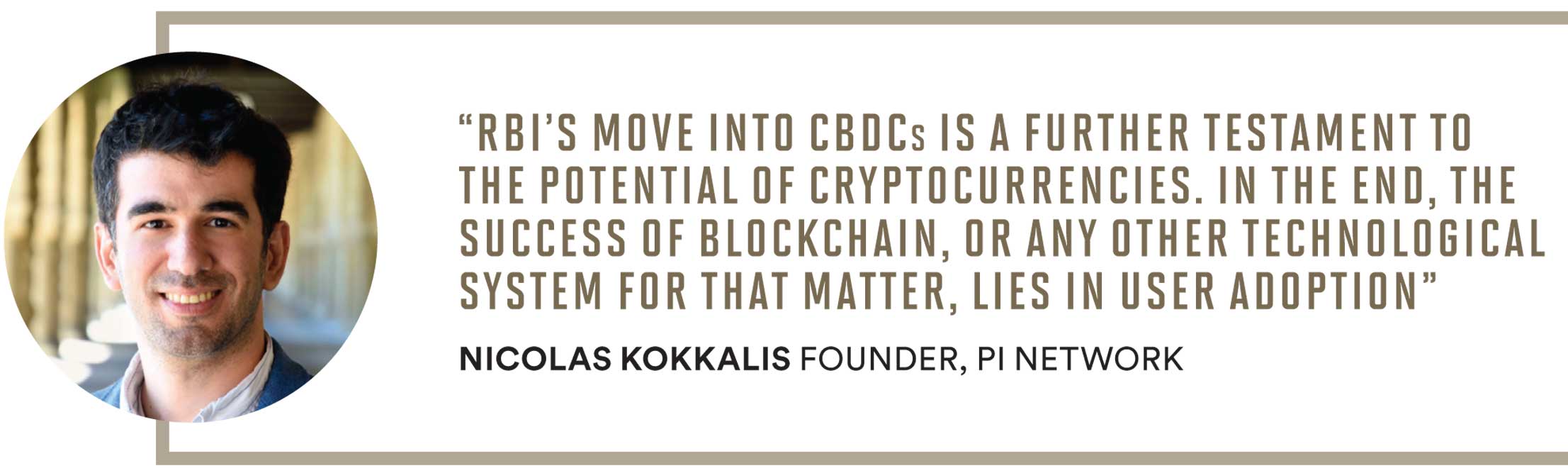

Nicolas Kokkalis, the founder and head of technology at Pi Network, the massive blockchain mining project that wants to offer everyone access to the cryptocurrency revolution, says, “There are many countries exploring the use of CBDCs, including a few pilot launches. Opinions vary on whether this is a sound monetary and financial policy or even an appropriate role for the government. It is not yet clear what characteristics the blockchains powering CBDCs will have, and how far beyond bank settlements CBDCs may be used.”

Kokkalis, a Stanford PhD, seems to derive a vicarious pleasure, though. “One thing is indisputable: blockchain is a powerful technology and it is here to stay. It is no longer an exclusive domain of a few tech nerds. The power of smart, programmable money has caught the attention of many enterprises and governments, and its impact can only be limited by one’s imagination.” Therefore, he says, the Reserve Bank of India’s move into CBDCs is a further testament to the potential of cryptocurrencies. He stresses, “In the end, the success of blockchain, or any other technological system for that matter, lies in user adoption. I believe making a currency accessible and useful to everyday people is key to its growth and relevance.”

RBI has not always been thrilled about the surge of cryptocurrencies and their acceptability. It had banned banks from facilitating crypto transactions earlier, a decision that was overturned in March 2020 by the Supreme Court of India. Incidentally, in this year’s Union Budget, India proposed a 30 per cent tax on all capital gains from digital assets and also added that a 1 per cent TDS will be charged on every transaction. Sanjeev Sanyal, then principal economic adviser, Ministry of Finance, wrote around the time in Open that what was imposed on gains on any asset sales and windfalls is reasonable. “When you buy and sell other assets, you have to pay capital gains tax. There is no particular reason why you shouldn’t be doing this for this particular asset. This does not endow any legitimacy to such crypto assets. It doesn’t in any way regulate or regularise this space. It just says what is obvious: if you make capital gains from other assets and pay tax, there is nothing exclusive about those who make a profit from crypto assets. Moreover, the current laissez-faire regulatory system cannot be sustained. Globally, the whole discussion on regulating crypto assets is taking place at the level of the G20 because it cannot be handled by any single country,” he wrote.

Bengaluru-based Sreejith Sreedharan, a former MNC banker and crypto enthusiast, dwells on the challenges ahead. He says, “At a base level, CBDCs are essentially upgrading current digital currency to more advanced, secure, and scalable blockchain technology, but minus decentralisation. While I understand the enthusiasm for CBDC, it comes with its own big challenges to address. While factoring in the huge advantages of cost, management, and administrative convenience of going fully digital, it, unfortunately, carries forward some of the fundamental flaws of fiat, too, like unlimited printing [made easier and cheaper now thanks to a few mouse clicks].”

ACCORDING TO HIM, the biggest challenge that needs to be comprehensively addressed about CBDCs is their potential to invade the privacy of citizens. “Cash and, to a good extent, digital currencies ensured that. I don’t want someone to know if I made a charitable donation or signed up on Tinder. We can’t wish away the inherent surveillance potential built into CBDCs. They are essentially programmable digital currencies. This has been publicly stated by many global financial regulatory and industry bodies. So, everyone working to introduce CBDC will follow those roadmaps, including the RBI. While I can understand the authorities’ mandate to track and prevent bad actors, surveillance on the whole population isn’t the answer.”

He notes that after reading the RBI’s concept note, he is confused about these two crucial aspects: “While the convenience of CBDC is unquestionable, the scope of its programmability is a cause for concern, if it is not adequately safeguarded through relevant new laws. Risk mitigation starts with charting out all possible risks, however extreme. It is like owning an autonomous Tesla car. It takes me everywhere in extreme comfort. However, at times, Tesla or some inimical hackers can take control of my car and drive me around or off the cliff! That’s not a comforting proposition. I would rather argue to maintain enough fiat currencies alongside CBDC.” Sreedharan hastens to add that even after all the fanfare about digital payments, especially using Unified Payments Interface (UPI), a large chunk of Indians use cash, which is still king. Less than 25 per cent of India’s population (discounting those under 14 years of age) has adopted UPI so far.

But then with many federal governments and central banks around the world stepping on the gas to get a huge stake in digital money, CBDCs have the momentum and institutional power on their side. The resilience of this digital currency, however, will depend on how smartly it is designed to meet people’s aspirations as well as address their concerns.